Bank of England 'firmly on track' to cut interest rates in March

The chances of a cut to UK interest rates next month have risen, following this morning’s data showing a rise in unemployment and a slowdown in wage growth.

The City money markets now indicate there’s a near-75% chance that the Bank of England lowers interest rates to 3.5% at its next meeting, in March, up from 69% last night.

Investors now fully expect two rate cuts by Christmas, which would bring Bank Rate down to 3.25%.

James Smith, developed markets economist at ING, says today’s UK jobs report keeps the Bank of England “firmly on track” for a March rate cut.

Smith says:

Unemployment is up and hiring surveys are still getting worse. That said, the weakness is still heavily concentrated in consumer-facing industries – a legacy of last year’s sizable payroll tax (National Insurance) and National Living Wage increases. Hospitality payrolled employment may be down almost 3% since the start of 2025, but it is still 2% higher than pre-Covid levels. Yet economic output is still 6% below – suggesting the loss of jobs may have further to run.

Outside of these consumer-centric industries, the story looks more benign. Employment is still trending down across the wider private sector on a three-month average of payrolls growth, but only slightly. We’re also not seeing a particularly noticeable pick-up in redundancies across the economy. Vacancy numbers have stopped falling, too.

Yael Selfin, chief economist at KPMG UK, says the fall in pay growth to 4.2% strengthens the case for a March interest rate cut:

“Today’s data raises the prospect of the Bank of England resuming cutting interest rates in March. The MPC will be reassured by further evidence of pay pressures easing, and the labour market continuing to soften. The Bank may also want to minimise downside risks to the labour market and lower rates ahead of the next forecast meeting in April.

“Headline pay growth eased in December, falling from 4.4% to 4.2%. The fall in headline pay was partly driven by an easing in public sector wage settlements, which fell for the first time since July 2025. Demand for labour remains weak which has curtailed workers’ bargaining power, meanwhile falling costs for households should also temper pay demand amongst workers. We expect pay growth to fall to 3% by the end of 2026.

Key events Show key events only Please turn on JavaScript to use this feature

Lisa O’Carroll

Irish exports surged to record levels in 2025 on the back of tariffs threatened by Donald Trump last March.

The 16% rise was largely driven by medical devices and pharmaceuticals made in Ireland by US and European multinationals including Pfizer, maker of Viagra, and Novo Nordisk, maker of Ozempic.

They accounted for more than 50% of all exports in the year.

Preliminary figures issued by the government’s Central Statistics Office, show the country exporters €260bn worth of goods in 2025 with the US the top destination market, followed by the Netherlands and Belgium where key ports Rotterdam and Antwerp/Bruges act as international shipping gateways.

Exports of medical and pharmaceuticals went up 39% to €138.9bn compared with €99.7bn in 2024 representing 53.2% of total exported goods in 2025.

Pharma and medical device companies rushed to export goods to the US in spring after Donald Trump threatened multiple tariffs on drugs made in Ireland.

He accused Ireland of stealing the US pharma industry at a St Patrick’s meeting with the Irish premier Micheál Martin last March.

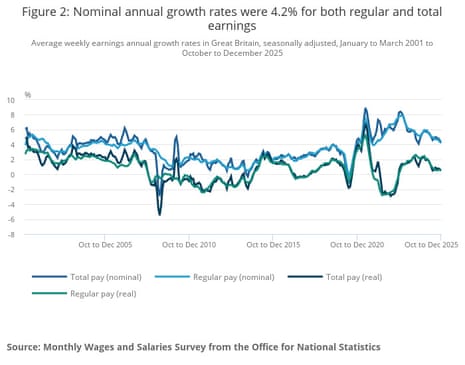

Charts: How UK pay growth has slowed

As is chart show, UK pay growth has slowed notably in recent months.

Regular pay (ie, excluding bonuses) growth has dropped to 4.2% in October-December 2025, down from 5.9% in the same quarter a year ago.

That has pushed down growth in real wages (ie, earnings after CPIH inflation) to just 0.5% in the final quarter of 2025, down from 2.4% in October-December 2024).

The weakness of the pound this morning helped to push the UK’s stock market towards a new record high.

The FTSE 100 share index rose as high as 10,528 points, up 54 points, only seven points off its all-time peak set last week.

A fall in the value of sterling typically boosts the share prices of multinational companies listed in London, as it makes their overseas earnings more valuable.

Fawad Razaqzada, analyst at City Index, says:

“The FTSE 100 edged higher to close in on last week’s record, as the pound weakened following the release of UK wages and Jobs data that puts a March rate cut firmly on the table, barring any surprises in tomorrow’s inflation report. Unless we see a sharp turnaround in data, I would be expecting another rate cut in June, and possibly more in the summer if inflation risks ease.

This should keep the longer term FTSE 100 forecast firmly supported and keep a lid on sterling.

Lisa O’Carroll

Shein has responded to the EU’s investigation, saying in a statement it took its obligations under the DSA “seriously”.

Shein says it has always cooperated fully with the European Commission and Coimisiún na Meán [the Irish regulator which will lead the investigation] and would “continue to” do so.

It added it had taken steps to limit harms, saying:

“Over the last few months, we have continued to invest significantly in measures to strengthen our compliance with the DSA. These include comprehensive systemic-risk assessments and mitigation frameworks, enhanced protections for younger users, and ongoing work to design our services in ways that promote a safe and trusted user experience.”

Cost of credit card borrowing hits 20-year high

The cost to borrow on a UK credit card has hit its highest level in at least 20 years, data provider MoneyFacts reports.

MoneyFacts data shows that the the average credit card purchase APR [annual percentage rate] hit 35.8% in February, the highest rate since records began in June 2006.

Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, says:

“The latest statistics from UK Finance reveal around half of credit card holders are now incurring interest charges, and while some might only owe a few hundred pounds, there will be others with significantly more debt that needs to be paid back. Luckily, there are some lengthy interest-free balance transfer cards to choose from, with TSB leading the market with a 38-month term, which charges a transfer fee of 3.49%. Reviewing card statements regularly is vital to stay on top of debts, but it’s also wise to make a calendar note of when any balances will incur interest. Shifting debts around is handy to grab interest-free offers, but the debt will hang overhead if only the minimum repayments are made each month.

“Not every borrower will have the best credit score, which is why it’s wise to check a credit report often before applying for a new card, and sort out any discrepancies. Those who get turned down will need to prioritise paying their debts as quickly as possible. Making fixed credit card payments is the fastest way to clear debts, those using a credit card charging 35.8% APR with a debt of £500 would take an entire year to pay it off based on a fixed repayment of £50, and it would cost £85 in interest. Increasing this payment to £100 per month would clear the debt in six months, and halve the interest charged (£42).

EU to investigate Shein over sale of childlike sex dolls and weapons

Lisa O’Carroll

Newsflash: The EU is to open a formal investigation into the Chinese retailer Shein over multiple suspected breaches of European laws including the sale of childlike sex dolls and weapons.

The European Commission said on Tuesday it had launched the inquiry after demanding information from the fast-growing company last year.

A senior EU official also pointed to reports of clothes, cosmetics, electronic products that were not compliant with EU law.

The investigation will examine three areas of Shein’s service that have given cause for concern.

Apart from the sale of illegal products, it will also look at the “addictive design of the service Shein is providing”, an EU official said, including bonus points programmes, gamification and rewards “that may lead to a risk of users’ mental well being”.

Smaller Christmas bonuses helped to depress pay growth in the last quarter of 2025, reports Andrew Wishart, senior UK economist at Berenberg bank.

He told clients:

“Employers play Scrooge: As companies no longer need to offer generous compensation to retain staff, they paid smaller Christmas bonuses than a year earlier. As a result, total pay growth slowed from 4.6% yoy in the three months to November to 4.2% 3m yoy in December (consensus 4.6%).

A sharper deceleration in pay growth than inflation cut real pay growth from 1.1% 3m yoy in November to 0.8% 3m yoy in December, its lowest since mid-2023. Alongside an increasing personal tax burden, we expect this to subdue consumer spending growth in the near term.”

And with slack increasing in the labour market, Wishart sees more chance of a cut to UK interest rates next week:

“Soft UK labour market data for December and January increase the chance that the Bank of England (BoE) will cut interest rates on 19 March already instead of waiting until the end of April as we forecast.

The tick up in the unemployment rate from 5.1% to 5.2%, another drop in payroll employment and still-elevated redundancies illustrate that the labour market continues to loosen.

Crucially, this fed through to a slowdown in pay growth - a critical variable for many Monetary Policy Committee (MPC) members looking for reassurance that labour market slack is causing wage inflation to ease.”

The UK’s youth unemployment crisis is worse than during the Covid-19 pandemic.

The jobless rate for 16-24 year olds has risen to 16.1%, over the peak recorded in 2020, and the highest since the end of 2014.

Barry Fletcher, chief executive at Youth Futures Foundation, flags that Britain’s youth jobless rate is now above the European average:

“The Office for National Statistics’ latest labour market data has been released today, showing that unemployment continues to increase at a rapid pace. Around 1 in 7 (14.1%) young people not in full-time education are now unemployed – up from 1 in 10 (10.0%) four years ago, when the UK was emerging from the pandemic. That means an estimated 469,000 16–24-year-olds not in full-time education are out of work and actively looking for a job. Over the past year, unemployment among young people has risen, while economic inactivity — those not in work and not actively looking — has fallen.”

“In the last few days, the OECD has highlighted that Britain’s youth unemployment rate has risen above the European average for the first time since records began in 2000. This not only demonstrates the scale of the issue we face, but that young people continue to bear the brunt of this labour market downturn.”

While we have recently seen much needed Government focus and investment to support more young people into work through employment support and apprenticeship reform, more will be needed to meaningfully tackle the youth employment challenge.

“As our Youth Employment 2025 Outlook reveals, the prize of sustainably addressing the UK’s stubborn employment challenge for our young people and the economy is enormous. If the UK matched the Netherlands’ youth participation rate, approximately 567,000 more young people would be in work or education, boosting the long-term economy by £86 billion.”

Britain’s weakening jobs market means the Bank of England will have to cut interest rates three times this year, predicts Tomasz Wieladek, chief European macro economist at asset management firm T. Rowe Price.

Today’s labour market data broadly confirms the MPC’s [monetary policy committee’s] recent dovish pivot. The unemployment rate rose to 5.2%, relative to expectations of 5.1%, while employment growth in the three months to December was 52k, below expectations of 108k. Payroll employment growth surprised to the upside, but remained in negative territory. All metrics indicate that the labour market continues to shed jobs. Wage growth is weakening and is now within a range consistent with achieving the inflation target.

At its last meeting, the MPC chose to put additional emphasis on labour market data in future monetary policy decisions. The data today show that the labour market is weakening slightly faster than expected. This is a result of both a jobless recovery due to the introduction of AI in the UK’s services-based economy and the fact that monetary policy is likely too tight to deliver the inflation target. The MPC will continue to react to these data developments.

I believe the MPC will cut at least three times this year. Financial markets still have to price this scenario. Sterling could weaken significantly against the US dollar again, and front-end gilts should rally from current levels.

Disappointingly, UK labour productivity deteriorated in the last three months of 2025.

The Office for National Statistics has estimated that output per hour worked in Quarter 4 2025 was 0.5% lower compared with Quarter 4 2024, while output per worker decreased by 0.2% compared with the same period.

The ONS says:

The information and communication industry made the biggest positive contribution to productivity growth, compared with the 2019 average; this was caused by a larger increase in gross value added (GVA) compared with hours worked.

Financial and insurance activities made the biggest negative contribution to productivity growth, compared with the 2019 average; this was caused by a small increase in the number of hours worked, alongside a more significant fall in output.

Company insolvencies rose in January

Another worrying development: the number of English and Welsh companies falling into insolvency rose by 4% in January, getting the new year off to a bad start.

HMRC data shows there were 1,744 registered company insolvencies in England and Wales last month, up from 1,683 in December.

On an annual basis, though, it’s 14% lower than in January 2025 (when there were 2,028 insolvencies).

HMRC reports:

Company insolvencies in January 2026 consisted of 256 compulsory liquidations, 1,323 creditors’ voluntary liquidations (CVLs), 151 administrations and 13 company voluntary arrangements (CVAs). There was one receivership appointment

Youth unemployment at joint 10-year high

The UK’s youth unemployment rate hasn’t been higher in a decade.

The 14% jobless rate recorded in October-December 2025 among the UK’s 18-24 year olds was last seen in July-September 2020, when Covid-19 lockdowns hit demand for workers.

To get a higher rate than 14%, you need to go back to April-June 2015 when it was 14.2%.

Louise Murphy, senior economist at the Resolution Foundation, says the UK’s unemployment problems need urgent attention:

At the end of last year almost one-in-six young people who wanted to work couldn’t find a job. Unemployment risks climbing even further in 2026.

“Many European countries have long grappled with high levels of youth unemployment and their efforts have pulled their rate below that of the UK. Getting youth unemployment down in this country – along with the share of young people who aren’t in education or training either – must be a top priority for 2026.”

Naomi Clayton, chief executive at the Institute for Employment Studies said:

“Unemployment is edging upwards as hiring remains weak. Payrolled employment continues to fall, though at a slower rate, and vacancies appear to have stabilised. Rising unemployment and weak hiring means that there are more people looking for fewer jobs and, outside the pandemic, the unemployment-to-vacancy ratio is the highest in 10 years.

Young people are being hit hardest, with youth unemployment at its highest in a decade. The government needs to work with employers to boost jobs and encourage hiring, while expanding support to help people find work.”

Full story: UK unemployment rate hits five-year high of 5.2% as wage growth cools

Tom Knowles

Unemployment in the UK has risen to 5.2%, the highest level in nearly five years, while wage growth continues to slow, raising the prospect of another cut to interest rates in the spring.

The Office for National Statistics (ONS) said the rate of unemployment was 5.2% in the three months to the end of December, the highest rate since the quarter to January 2021. This was in line with what economists had been expecting and was up from 5.1% in the three months to November.

Joblessness in the UK has steadily risen since 2022, and businesses have complained that tax rises by Rachel Reeves in her last two budgets have exacerbated this, with rises in national insurance contributions and the minimum wage causing particular issues.

In the three months to December, wages excluding bonuses in Great Britain increased by 4.2%, easing from 4.4% the previous month.

In the private sector, pay rose by 3.4%, the lowest level in five years, while wages in the public sector rose by 7.2%. Once adjusted for inflation, annual pay excluding bonuses rose by just 0.8% in October to December, the lowest rate since August 2023.

The number of people on company payrolls also continued to fall, down 134,000 on a year ago, and by 46,000 over the quarter. On a monthly basis, payrolls fell by 11,000 in January.

UK bond yields drop

UK government borrowing costs are dropping this morning, as the weakening jobs market puts pressure on the Bank of England to cut interest rates.

The yield, or interest rate, on two-year UK gilts has dipped by two basis point (0.02 percentage points) this morning. That’s a small move, reflecting the increased expectations of a rate cut in March.

The yield on benchmark 10-year gilts is down 2 basis points too, to 4.368%. That’s a one-month low, eliminating the rise in borrowing costs during the political furore over Keir Starmer’s future earlier this month.

That will be welcomed by the government, as it indicates that the cost of servicing the national debt has dropped.

Yesterday, Bloomberg reported that chancellor Rachel Reeves is on track to bank an extra £1.5bn in lower borrowing costs at her spring statement in March, compared to her budget last November. That’s because yields on 10-year gilts have fallen 25 basis points over that time.

Unemployment rises: the political reaction

Work and Pensions Secretary Pat McFadden says the government is taking steps to help young people into work:

“Today’s figures show there are 381,000 more people in work since the start of 2025, but we know there is more to do to get people into jobs.

“Our £1.5 billion drive to tackle youth unemployment is a key priority and this month we announced that we’ll make it easier for young people to find and secure an apprenticeship, which comes on top of our investment to create 50,000 new apprenticeships.”

But Shadow work and pensions secretary Helen Whately blames the government for fuelling the youth unemployment crisis:

“An unprecedented series of monthly unemployment increases is the hallmark of this Labour Government.

“The predictable result of bad decisions and economic incompetence.

“Young people are taking the hardest hit. Entry-level roles are the first to disappear from Labour’s tax hikes. By making hiring more expensive and more risky, Labour have are ensuring school leavers and graduates never even get a foot in the door.”